The Iran War: Impact of Rising Crude Oil Prices on Nigeria’s Mineral Revenue

Since the outbreak of the third Gulf War in Iran on 28 February, the price of Brent has risen from $72.87 to over $100, reaching $107.39 on 18 March – a 47% increase. An estimated 25% of the world’s seaborne oil trade has been disrupted by this war due to attacks on the Strait of Hormuz, through which Gulf countries, including Bahrain, Qatar, Iran, Iraq, Kuwait, Saudi Arabia and the United Arab Emirates, export an average of 20 million barrels per day (mb/d) to the global oil market.

Besides attacks along the shipping route, there have been assaults on energy infrastructure, including the Ras Tanura and SAMREF refineries in Saudi Arabia, storage facilities in the Shah gas field in the United Arab Emirates, the Ras Laffan LNG complex in Qatar, and the Mina al-Ahmadi refinery in Kuwait. Even if the war ends and the Strait of Hormuz “reopens”, a recovery will require restoring oil output to pre-war levels. This will depend on the extent of damage to these oil facilities.

For oil-exporting countries like Nigeria, rising oil prices can result in higher net oil export earnings, increased foreign reserves, accretion to the government’s federation account, and excess crude savings if the government chooses to save for rainy days. Multiple knock-on economic and fiscal implications are also expected, including a sharp rise in premium motor spirit (PMS) in an industry now deregulated, as well as higher energy and transport costs, with multiplier effects on living and production costs for households and businesses, respectively.

This note does not discuss these multiplier effects but focuses on the impact on government revenue, i.e. mineral (oil) revenues remitted to the federation account and shared monthly to the three tiers of government

What does the increase in oil prices mean for Nigeria’s mineral revenues?

This analysis is based on the federal government’s 2026 budget benchmark price of $65 per barrel and an exchange rate of ₦1400 per US dollar. The budget assumes an optimistic production target of 1.84 million barrels, but this analysis is built on a conservative production capacity of 1.7 million barrels per day in 2026, following an average of 1.65 MBPD in 2025, including unblended condensate.

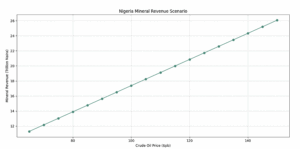

At a crude oil production level of 1.7 million barrels per day and an exchange rate of ₦1,400 per USD, Nigeria’s mineral revenue is expected to rise by ₦72.4 billion each month (₦868.7 billion annually) for every $5 increase in global crude oil prices. The federation’s mineral revenue can potentially rise to ₦14.8 trillion at an average oil price of $85 per barrel in 2026, ₦20 trillion at $115 per barrel, or ₦26 trillion at $120 per barrel (see table 1). For State governments, this translates to ₦26.19 billion in additional monthly inflows for each $5 increase in crude prices – monies that can be invested in infrastructure (power and roads), education, and health, to foster economic productivity and social welfare.

Over the last three years, the country’s mineral revenues have increased by more than 100%, rising from ₦4.9 trillion in 2023 to ₦10 trillion in 2024 and reaching ₦12.2 trillion in 2025. This growth followed the free-floating of the Naira in May 2023, which saw the currency’s value against the dollar decline from ₦460 in early 2023 to a range of ₦1,500 to ₦1,600 in 2025.

Table 1: Scenarios for Nigeria’s Mineral Revenue in 2026

| Scenario | Oil Price Range | Revenue Range (Annual) |

|---|---|---|

| Base Case | $65–85 | ₦11.3T – ₦14.8T |

| Scenario II | $90–115 | ₦15.6T – ₦19.98T |

| Scenario II | $120–150 | ₦20.8T – ₦26.1T |

Figure 1: Scenarios for Nigeria’s Mineral Revenue in 2026

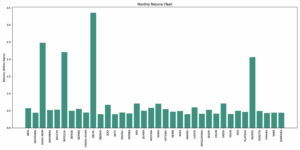

Figure 2: Monthly Returns from a $5 increase in Crude Price

Higher oil prices will bring about fiscal gains for all tiers of government, especially oil-producing States through derivation (see figure 2), but these gains are subject to volatility from currency fluctuations and production changes. Any sustained escalation in the conflict can drive further price increases but could also disrupt supply chains, heighten market uncertainty, or prompt oil producers to make compensatory production decisions to moderate price effects. As a result, State governments are encouraged to treat such windfalls as temporary and to integrate them cautiously into medium-term budget planning.

To prevent long-term budget risks, governments must not increase their permanent recurrent revenues to correspond with temporary windfalls.

One of the main challenges State governments face is how to stabilise their budgets and maintain healthy fiscal balances. Unlike the federal government, most States do not have a stabilisation fund to help smooth cyclical fluctuations in revenues. Fewer than half maintain a sinking fund to secure the debts they incur. State budgets have risen sharply in the last two years, from under ₦10 trillion pre-2023 to over ₦26 trillion in 2025, owing mainly to the free-floating of the Naira, which doubled returns from dollar-denominated revenues (including mineral revenues). With limited headroom to restore fiscal balance or implement stabilisation policies, there is a risk of an impending debt overhang, as was the case during the 2016 recession. Between 2014 and 2018, total public debts for both the federal and State governments had more than doubled from ₦11.2 trillion to ₦24.4 trillion. During the period, the domestic debts of States grew by a compound annual rate of 23% from ₦1.7 trillion to ₦3.9 trillion. Many States had, in fact, borrowed from their staff, pensioners and suppliers by accumulating significant arrears