Digitalising Revenue Administration: Lessons for Nigeria.

One of the challenges revenue authorities face is delivering digital transformation quickly and cost-effectively. This is especially difficult for governments with fragmented digital ecosystems, where multiple vendors operate separate services and data standards limit interoperability.

For many States, the systems used to register taxpayers, issue bills, and collect payments are spread across multiple platforms. This fragmentation makes it harder for citizens and businesses to pay taxes, slows internal operations, and increases the risk of errors and leaks.

This digital fragmentation is a product of siloed digitalisation, where different agencies procure bespoke solutions at different times without a central architectural blueprint. While these systems may solve immediate organisational needs, they inadvertently create parallel high-maintenance systems that operate in isolation.

This is a note for governments, based on lessons from NGF’s Digital Public Infrastructure (DPI) and Intelligent Revenue Authority (IRA) reports for Nigeria and a digital tax assessment of Kaduna State, Nigeria. It identifies actions States can take to accelerate the transformation of their revenue systems.

Digital systems and processes

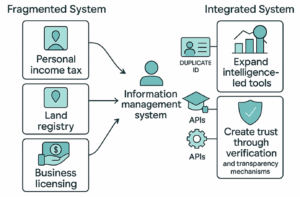

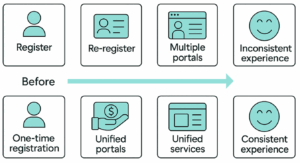

For these governments, the cost of digital fragmentation is the loss of agency to integrate data and simplify business processes. Within the revenue service, this takes the form of multiple systems for different functions, such as personal income tax, property tax, business licensing, motor vehicle licensing, gaming, and the collection of fees, fines, and levies. As a result, taxpayers visit multiple portals, register more than once, and navigate inconsistent interfaces, which increases the compliance burden.

Interoperability and data exchange

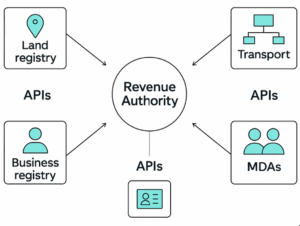

Outside the revenue service, fragmentation manifests as “islands of data” across line ministries, departments, and agencies (MDAs). Revenue authorities rely on data held by identity registries, land registries, transport agencies, business regulators, financial intelligence units, and MDAs that issue permits and licences. Interoperability is weakest where data sharing is manual, requiring letters, flash drives, or requests that can take weeks or months to fulfil.

Only a few States have automated systems or secure file transfer arrangements. Without regular, structured data flows, authorities may be unable to cross-verify declarations, detect discrepancies, or proactively identify non-compliance at scale. This limits the effectiveness of digital tools for functions such as identity verification, risk profiling, behavioural nudges, and analytics-driven revenue forecasting.

For example, the Ministry of Commerce maintains a database of registered businesses, while the Land Bureau operates a closed geographic information system (GIS) for land and property data. Because these systems are traditionally built on proprietary software with incompatible data structures, they cannot communicate with the revenue administration system without an Extraction, Transformation and Loading (ETL) process.

Even where systems are connected within States, they may not reliably interpret data from other States, especially when fewer than half of the States in Nigeria share common metadata and terminology standards. Only 20 revenue authorities present their web resources in XML or JSON formats. Without shared data standards and common machine-readable formats, automated information exchange among agencies and States will be technically challenging.

One way to solve this problem is to adopt the Nigeria e-Government Interoperability Framework (Ne-GIF), which provides guidelines and standards to promote seamless data exchange and service integration across government agencies and departments in Nigeria.

| Ne-GIF Standard | Compliance Level | Strategic Importance |

|---|---|---|

| Operating Systems (POSIX) | 24 States | Foundational stability & security. |

| Data Formats (XML/JSON) | 20 States | Language for data exchange. |

| Web Service Modelling Ontology (WSMO) | 19 States | Ability to deploy advanced web services. |

| Metadata Standards | 15 States | Accuracy of inter-agency data sharing. |

Source: Nigeria – DPI Readiness of States: The Intelligent Revenue Authority (IRA) Readiness Report, 2025

This lack of interoperability makes it difficult to achieve end-to-end visibility of taxpayer activities across platforms. Without secure links to non-revenue systems, such as government contractor payment platforms, the authority may be unable to verify a taxpayer’s economic footprint or automate the issuance of Tax Clearance Certificates (TCCs). A fragmented non-revenue ecosystem locks the authority into manual data entry and reconciliation, which is costly and increases control risks that modern digital public financial management (PFM) aims to reduce.

Identity data foundations

Another challenge is weak identity and entity data foundations. Without reliable identity anchors, such as the National Identification Number (NIN) for individuals, the Corporate Affairs Commission (CAC) Registered Company (RC) number for limited liability companies, and the Business Name (BN) for sole proprietorships or partnerships, revenue systems cannot enforce real-time validation at the point of registration. This creates loopholes for fictitious or duplicate taxpayer profiles, degrades data quality, and weakens the accuracy of assessments. It also makes it harder to automate onboarding, link datasets across MDAs, and apply risk-based profiling.

There is some progress. 23 States have linked individuals’ tax IDs to their NINs via rule-based APIs, while 16 States have extended this capability to businesses via the CAC. The majority attribute the slow pace of accessing the country’s national identity databases to fee-based API calls and system incompatibility.

Inclusivity and payment access

While online payment gateways are widely used, large segments of taxpayers, particularly in rural or informal sectors, lack seamless access due to low digital literacy, unreliable connectivity, or a preference for cash-based transactions. When payment platforms do not support Unstructured Supplementary Service Data (USSD), Interactive Message/Voice Response (IMR/IVR), mobile money, or instalment payments, this prolongs reliance on manual processes or third-party intermediaries, which are potential points of revenue leakage.

Digital skills and governance capacity

In many cases, IT units are understaffed and not sufficiently trained in emerging disciplines such as Application Programming Interface (API) management, cybersecurity, data science, cloud computing, Extract, Transform, Load (ETL) processes, machine learning, and user-centred design. There is also a shortage of expertise in disciplines such as project management, procurement, and contract management. This results in dependence on external vendors, reduces oversight of system architecture, and weakens quality assurance during contracting and upgrades. When internal administrative functions such as records management, workflow approvals, and audit trails remain paper-based, they also become bottlenecks that undermine the benefits of digital taxpayer-facing systems.

Legal and procedural alignment of legacy systems

Several legacy digital systems do not reflect updated federal or state tax laws, particularly regarding assessment rules, objections, appeals, tax clearance certificate (TCC) timelines, withholding obligations, and instalment payments. Without ensuring legal compliance in digital workflows, authorities risk disputes, operational inconsistencies, and taxpayer dissatisfaction.

How revenue administration can evolve

Digital Public Infrastructure (DPI), which generally refers to secure digital identity, interoperable data exchange, and inclusive payments, has the potential to deliver essential digital functions at scale and enable public and private service providers to reuse these systems, innovate, and roll out new services more quickly and efficiently across sectors. The following 10 actions are ways to adopt this new way of thinking.

Digitalising Revenue Administration

| Digital Public Infrastructure Digital identity • Data exchange • Digital payments |

|

|---|---|

| Taxpayer-facing | Internal administration |

| • Unified taxpayer account (secure customer account (SCA) / single sign-on (SSO)) • Identity validation (NIN/BVN, CAC) • Smart filing & assessment features • Rights-based compliance (objections/appeals) • Inclusive, omnichannel payments • Public verification tools |

• Digitised workflows and document management • Role-based access controls and audit trails • Risk-based analytics and forecasting • Digital skills and governance capacity |

| Automate compliance processes | Automate role-based processes |

1. Audit and build an integrated, unified revenue ecosystem

Carry out an audit of all digital platforms for PIT, road taxes, stamp duty, property taxes and other MDA revenue collections, to identify duplicate registrations, inconsistent taxpayer journeys, and administrative inefficiencies.

- Consolidate all revenue functions under a single secure customer account (SCA) and single sign-on (SSO) architecture.

- Integrate legacy systems through APIs rather than maintaining parallel platforms.

- Avoid redirections between websites; one login should unlock all compliance functions and obligations.

2. Anchor registration on foundational digital identity

Introduce real-time identity validation at the point of taxpayer onboarding to protect the integrity of the taxpayer database.

- Introduce NIN/BVN (for individuals) and CAC RC/BN (for business entities) validation at registration.

- Do not treat identity numbers as “optional” or post-registration sync fields.

- Consolidate multiple taxpayer IDs (e.g., internal IDs, TIN/TIN-like numbers) into one permanent tax identity.

3. Prioritise data interoperability across government

Revenue systems gain intelligence when connected to the rest of the government.

- Use APIs, Secure File Transfer Protocol (SFTP), and secure integrations to connect with land/property registries, business registries, payment platforms, financial intelligence data, and MDA licensing systems.

- Build data sharing agreements to eliminate silos and increase the accuracy of registries, assessments, audits, and enforcement.

4. Improve filing and assessment through smart features

Digital systems can be difficult to navigate if poorly designed.

- Provide hover tooltips, field-level explanations, and examples in filing pages.

- Implement smart data pre-filling to reduce repetitive data entries.

- Ensure automated calculation engines reflect current tax laws and rates.

- Expand filing functionality to support document upload and data transformation to fill input fields.

5. Strengthen rights-based compliance modules

Digital transformation must enforce taxpayer rights and statutory processes.

- Redesign objections modules to capture all details required by law, including disputed amounts, justification, proposed corrections, and income/tax admitted.

- Automatically enforce statutory timelines (e.g., 30-day objection window, 90-day response by the authority).

- Provide a transparent tracker so that taxpayers know the status of objections.

6. Enable inclusive and omnichannel digital payments

Digital payment systems must work for both highly connected urban users and informal/rural taxpayers.

- Integrate online gateways and complement them with USSD payments and mobile money or agent-assisted channels

- Support instalment payments, with automated reconciliation and clear reporting for taxpayers.

- Maintain functioning IMR/IVR and chatbot-style assistance for real-time support.

7. Improve transparency with public verification tools

Trust is strengthened when taxpayers can independently verify those who assess or collect revenue.

- Introduce a public portal that verifies staff identity, taxpayer IDs, invoices, demand notices, and receipts to reduce fraud risk and increase compliance confidence.

8. Digitise internal workflows to complement taxpayer interfaces

Many States tend to prioritise taxpayer-facing processes over internal processes.

- Deploy a workflow and document management platform for personnel files, internal memos, approvals, and audit trails.

- Integrate role-based access controls and notifications/reminders.

9. Build capability for predictive and risk-based revenue administration

Modern revenue authorities are intelligence-led.

- Use machine learning and rules engines to detect anomalies and support Best of Judgement Assessments.

- Implement risk-based profiling and audit selection using historical data and variance rules.

- Build dashboards that present data by sector and comprehensive demographic segmentation, moving average revenue forecasting and performance monitoring.

10. Invest in the digital skills of staff

Technology is only as effective as the people using it.

- Establish continuous learning programmes in DPI, API management, data science, Extract, Transform, Load (ETL), cloud computing, cybersecurity, user acceptance testing, systems administration, project management, procurement and contract management.

- Reduce reliance on external consultants by strengthening internal IT units.

Making tax digital is a system-wide, multi-institutional, all-of-government effort that goes beyond deploying another new software for tax administration. It will require shared data standards, interoperable platforms, harmonised laws and processes, and sustained change management across MDAs. It is tedious and incremental.